What we Acquire

Abode Harmony acquires real estate (and most capital assets) interests and aligns the transactions to accommodate the owners' business and financial objectives

1Disposition

Asset disposition structured to defer recognition of gains as confirmed by your tax advisors.

2Liquidity

Receive cash proceeds in an amount equal to a mutually-agreed value.

3Donation

Donate all or a percentage of the asset; while reducing your corporate, income, estate and/or capital gains tax.

Deferred Benefits

The benefits of delaying recognition of gains, for 30 years or more after removing the asset from your books, are numerous. This immediate cash windfall and huge savings on the year one tax bill contributes more funding towards your objectives. For example, you can choose to invest the portion of profit that would have gone to taxes in year one, as shown below.

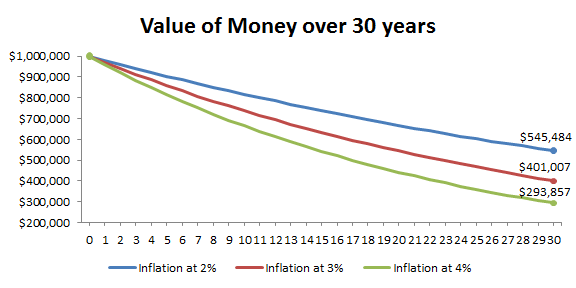

Inflation depreciates the Value of Money!

Inflation reduces the purchasing power of money drastically over time. For example, a one million dollar purchase 30 years from now would be about 45.5% less than what one million dollars would purchase today, at 2% average inflation.

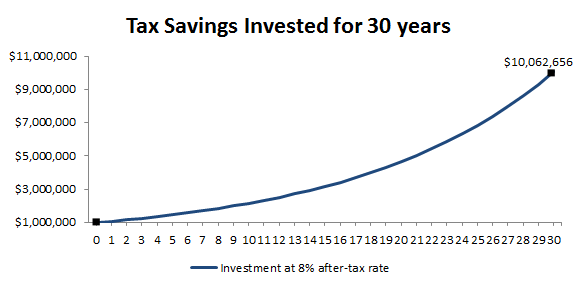

Invest the Cash Windfall!

Over the last century, the stock market has earned at least 8% annual returns in any 30 year period including the great depression. If history repeats, the gains will be more than 10 times the tax owed.

Case Studies

- Purchase

- Donation

- Debt-Over Basis

-

A comparison of Abode Harmony acquiring the asset versus a 3rd party buyer is shown below. Karen wishes to sell an asset for $5 million and has a tax basis of zero dollars. Karen's combined state and federal taxes owed is approximately 30%. Abode Harmony's transaction concludes after 30 years. Transaction costs are not taken into account in this study.

-

A comparison of Abode Harmony acquiring the asset versus a 3rd party buyer is shown below. The results of donating ten percent ownership of the asset versus donating ten percent of the cash proceeds is also displayed. Mark, the owner, wishes to sell the asset for $10 million and has a tax basis of zero dollars. Mark's combined state and federal taxes owed is approximately 30%. Abode Harmony's transaction concludes after 30 years. Transaction costs are not taken into account in this study.

-

Owners of encumbered assets with very low tax basis have a dilemma. After the existing debt is paid at closing, their tax cost may exceed profit and will have to come out-of-pocket to settle the overage. For example, Greg purchased a property that has doubled in value to $20 million after 15 years of ownership. He took a loan out for 50% of its value or $10 million which lowered his tax basis to zero. Unfortunately, the asset's market value dropped to $14 million, a year later. Greg combined state and federal taxes owed is approximately 40%. Abode Harmony's transaction concludes after 30 years. Transaction costs are not taken into account in this study.

-

A: Cash Sale

The asset sells for $14 million to a 3rd party buyer. Greg pays $1.6 million out of pocket for taxes, the following year after the sale.

Gross proceeds $ 14,000,000 Mortgage - 10,000,000 Net proceeds, year 1 4,000,000 Tax due, year 1 - 5,600,000 Out-of-pocket cash, year 1 -1,600,000 -

A: Cash Sale

The asset is sold for $5 million to a 3rd party buyer. The capital gains taxes owed is approximately $1.5 million. Karen earns $3.5 million after taxes.

Gross proceeds $ 5,000,000 Tax due, year 1 - 1,500,000 Net proceeds, year 1 3,500,000 Cash sale differential - Invest 30 years @ 3% - Tax due, year 30 - Profit, year 30 - -

A: Cash Sale

A 3rd party buyer purchases the asset for $10 million. The capital gains taxes owed is approximately $3 million. One million dollars is donated to charity which saves $300,000 in taxes. Mark earns $6.3 million.

Gross proceeds $ 10,000,000 Less gift - 1,000,000 Tax Benefit + 300,000 Tax due, year 1 - 3,000,000 Net proceeds, year 1 6,300,000 Cash sale differential - Invest 30 years @ 3% - Tax due, year 30 - Profit, year 30 - -

Asset Eligibility

Abode Harmony purchases highly appreciated capital assets. These assets must have a minimum value of $500,000 but there isn't a maximum value limit.

-

B: Abode Harmony

Abode Harmony acquires the asset for $13.3 million. Greg pays $2,219,500 out-of-pocket for taxes, 30 years after the transfer.

Gross proceeds $ 13,100,500 Mortgage - 10,000,000 Net proceeds, year 1 3,100,500 Tax due, year 30 - 5,320,000 Out-of-pocket cash, year 30 -2,219,500 -

B: Abode Harmony

Abode Harmony acquires the asset for $4.75 million. Karen receives 98.5% of this amount and earns over $6.1 million after investing the tax windfall.

Gross proceeds $ 4,678,750 Tax due, year 1 - Net proceeds, year 1 4,678,750 Cash sale differential 1,178,750 Invest 30 years @ 3% 2,861,135 Tax due, year 30 - 1,403,625 Profit, year 30 1,457,510 -

B: Funding pre-Donation

Abode Harmony acquires the asset for $9.5 million with Mark receiving 98.5% of this amount after funding costs. One million dollars is donated to charity. Mark earns $11.57 million over the 30 year period.

Gross proceeds $ 9,357,500 Less gift - 1,000,000 Tax Benefit + 300,000 Tax due, year 1 - Net proceeds, year 1 8,657,500 Cash sale differential 2,357,500 Invest 30 years @ 3% 5,722,271 Tax due, year 30 - 2,807,250 Profit, year 30 2,915,021 -

Assets Accepted

Most capital assets are eligible for purchase. However, assets traded on public exchanges aren't eligible. The assets may include commercial & residential real estate, business entities, professional practices and much more.

-

Summary

As shown, Greg has capital to spend how he desires, after transferring the asset to Abode Harmony. He can invest this windfall to help pay the $5.32 million tax due in 30 years. Alternatively, Greg would pay $1.6 million out-of-pocket to cover the costs of selling, within a year after the asset is sold to another buyer.

*This case study is for illustration and discussion purposes only. It is not intended to be, nor should it be construed or used as, investment, tax or legal advice; viewers must consult with their own professional investment, tax and legal advisors. -

C: Donation pre-Funding

Ten percent ownership is donated to charity. Abode Harmony acquires the asset for $8.55 million with Mark receiving 98.5% of this amount after funding costs. Mark earns $12.07 million over the 30 year period.

Gross proceeds $ 8,421,750 Gift (10% ownership) - Tax Benefit + 300,000 Tax due, year 1 - Net proceeds, year 1 8,721,750 Cash sale differential 2,421,750 Invest 30 years @ 3% 5,878,222 Tax due, year 30 - 2,526,525 Profit, year 30 3,351,697 -

Summary

Abode Harmony's acquisition results in higher proceeds to fund projects in the short and long term for Karen. In this case, Karen chose to invest the tax windfall (and earned a 3% after-tax rate) over 30 years. The capital gains taxes are paid with dollars that have significantly lost their value due to inflation.

*This case study is for illustration and discussion purposes only. It is not intended to be, nor should it be construed or used as, investment, tax or legal advice; viewers must consult with their own professional investment, tax and legal advisors. -

As illustrated, Mark's best outcome is donating an ownership interest in the asset. More proceeds are earned to fund projects in the short and long term. Mark chose to invest the tax windfall (and earned a 3% after-tax rate) over the 30 year period. The capital gains taxes are paid with dollars that have significantly lost their value due to inflation.

*This case study is for illustration and discussion purposes only. It is not intended to be, nor should it be construed or used as, investment, tax or legal advice; viewers must consult with their own professional investment, tax and legal advisors.

CONTACT US

Coming Soon

** Disclaimer - Abode Harmony and employees do not provide tax, legal and financial advice, and these materials and statements contained herein should not be construed as tax, legal or financial advice. Readers are urged to consult their personal tax advisor or attorney for matters involving taxation and tax planning, financial advisors for matters concerning financial planning and their personal attorney for matters involving trust and estate planning and other legal matters.